Here’s a number that should stop you mid-scroll: according to NIH Research Matters, 42% of Americans over age 55 will eventually develop dementia, a figure more than double what researchers previously projected. That single stat is why long-term care insurance for cognitive decline has become one of the most searched, most debated, and most misunderstood corners of the insurance world, and our 2026 market analysis breaks down exactly what’s changed, what it costs, and what actually helps.

| Question | Quick Answer |

|---|---|

| Is long-term care insurance for cognitive decline worth it in 2026? | Yes for most middle-income households, given average lifetime dementia care costs now stretch into six figures. |

| What’s driving the 2026 market analysis findings? | Rising life expectancy, updated dementia risk models, and higher paid claims are pushing insurers to reprice policies aggressively. |

| Does insurance cover memory care specifically? | Most hybrid and traditional LTCI policies cover memory care facilities, in-home dementia care, and adult day programs. |

| Can brain training reduce my future care needs? | Growing evidence suggests it can help delay decline; see our breakdown of cognitive training vs. memory apps for seniors. |

| Who pays more for coverage, men or women? | Women pay significantly more because they live longer and use care longer on average. |

| When should I buy a policy? | Most advisors recommend locking in coverage between ages 50 and 65, before health changes trigger higher premiums or denials. |

| What’s the biggest mistake families make? | Waiting until a diagnosis to shop for coverage, at which point most insurers will decline the application entirely. |

Dementia is no longer a rare, late-life event that catches a few unlucky families off guard.

It’s a mainstream financial risk that touches almost half of older adults, and the 2026 market analysis reflects that shift in real dollars.

The USC Schaeffer Center now estimates the total cost of Alzheimer’s disease and related dementias to the United States at $818 billion in 2026, covering medical care, long-term care, and diminished quality of life.

That’s not an abstract federal budget line. It’s the sum of thousands of individual families paying for memory care facilities, home health aides, and lost income while caring for a loved one.

The immense financial burden of cognitive decline makes long-term care insurance a critical financial safeguard for families.

Let’s talk numbers, because this is where the 2026 market analysis gets uncomfortable fast.

Milliman projects the average lifetime long-term care cost for a 65-year-old female at $171,000, roughly 75% higher than the $98,000 projected for males.

Why the gap? Women simply live longer and need care for a longer stretch of years, which is exactly why insurers price female applicants differently.

For anyone requiring extended long-term care of five years or more, that number balloons dramatically.

Milliman’s data shows the average total cost for extended care cases hits $665,000, which is precisely why so many financial advisors now treat long-term care insurance for cognitive decline as a non-negotiable line item in retirement planning.

Those figures don’t include the hidden cost of unpaid caregiving, either. Family members and friends provided an estimated 6.8 billion hours of unpaid dementia care in 2026 alone, valued at roughly $237 billion.

Insurers aren’t sitting still while these numbers climb.

Milliman projects that annual paid long-term care insurance claims will peak around $44 billion by 2041, with the number of policyholders actively on claim expected to hit 332,000 by 2037.

That’s a long runway of rising liability, and carriers are responding with tighter underwriting, higher premiums for cognitive risk factors, and more hybrid life/LTC products that build in a death benefit if care is never needed.

If you’re comparing quotes this year, expect medical underwriting to ask pointed questions about family dementia history, current cognitive screening scores, and lifestyle factors tied to brain health.

Carriers are increasingly rewarding applicants who can show proactive brain health habits, from regular cognitive assessments to documented preventative routines, when calculating premiums for cognitive decline coverage.

Insurance is only half the equation.

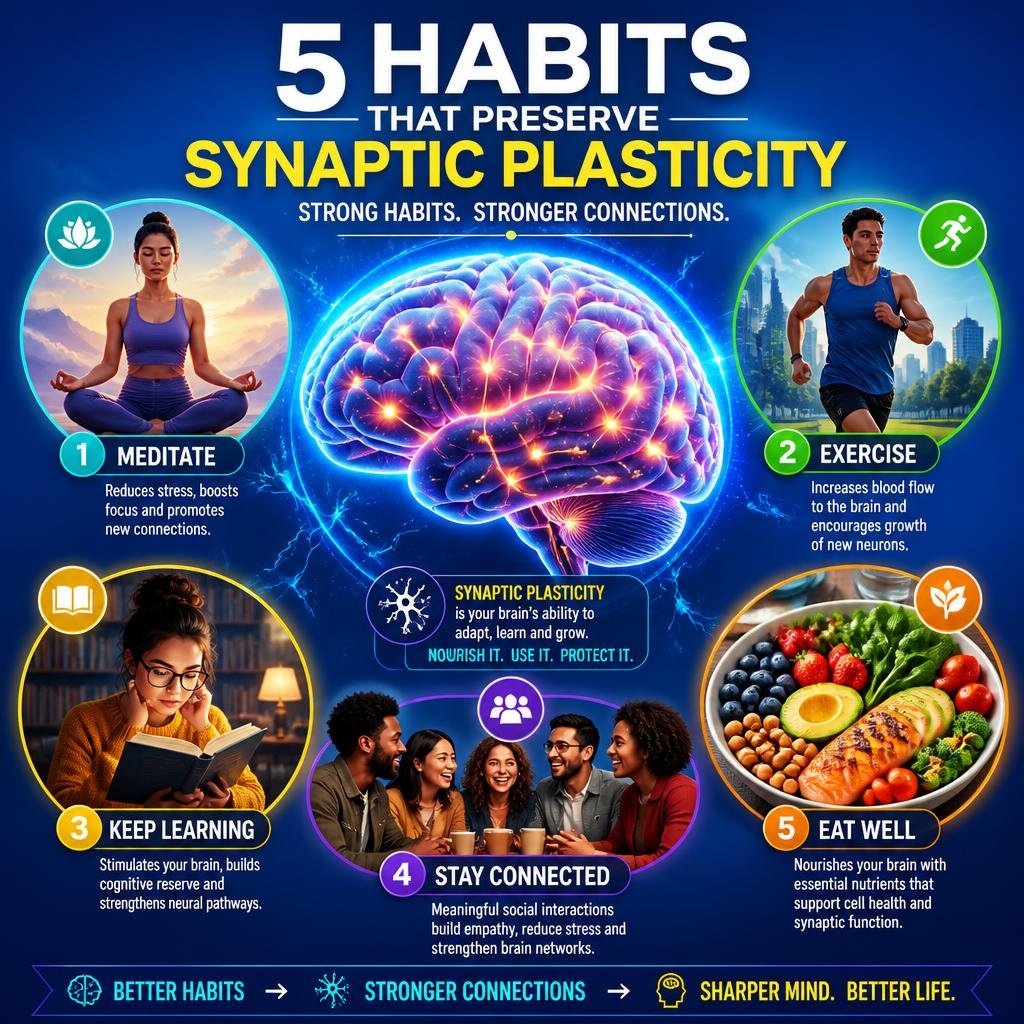

The other half is doing everything reasonable to delay the decline in the first place, and this is where manifestation techniques, BDNF activation, and BrainWave-style protocols to boost brain power naturally have gained real traction among people trying to protect their long-term cognitive health.

Brain-Derived Neurotrophic Factor, or BDNF, acts like fertilizer for your neurons.

It encourages the growth of new synapses and protects the ones you already have, and it responds directly to aerobic exercise, cognitive challenges, and targeted nutrition.

People pairing manifestation techniques with structured BDNF-boosting routines and BrainWave audio protocols report better focus and mood stability, which insurers increasingly view as favorable data points during underwriting.

We’re not saying visualization exercises replace a policy.

We’re saying that combining manifestation techniques, BDNF-focused habits, and BrainWave stimulation to boost brain power naturally can meaningfully change your risk profile over decades, which matters when you’re the one paying the premium.

Preventative longevity isn’t a fringe idea anymore.

58% of consumers now say they’re interested in visiting specialized longevity clinics for personalized health assessments, up from just 40% in 2021, which tells you where this conversation is heading.

Even in an aging brain, the hippocampus (the region responsible for learning and memory) keeps producing new neurons.

Those new cells need the right environment to survive, and that’s the whole point behind modern cognitive longevity programs.

Some of the most-discussed tools in this space right now include:

These strategies won’t eliminate your risk of cognitive decline, but they support the broader case for long-term care insurance for cognitive decline: the 2026 market analysis shows premiums are lower and approval rates higher for applicants who can demonstrate consistent brain-health habits over time.

Every family we talk to eventually asks the same question: do memory apps actually work, or is structured cognitive training the better investment?

The honest answer is that it depends on consistency and design, not just the label on the app.

Structured cognitive training programs tend to use adaptive difficulty and multi-domain challenges (memory, processing speed, executive function), while many consumer memory apps focus narrowly on one skill.

If you want a deeper side-by-side breakdown, our full comparison of cognitive training programs versus memory apps for seniors walks through which formats show measurable results and which are mostly entertainment with a brain-health label attached.

Did You Know?

Family members and friends provide an estimated 6.8 billion hours of unpaid dementia care every year, valued at approximately $237 billion, according to the USC Schaeffer Center.

Not all policies are built the same, and this matters enormously once cognitive decline enters the picture.

Here’s what we recommend comparing before you sign anything:

| Policy Feature | Why It Matters for Cognitive Decline |

|---|---|

| Cognitive impairment trigger | Confirms benefits activate based on cognitive test scores, not just physical ADL limitations. |

| Inflation protection | Protects your daily benefit amount against rising memory care facility costs over a 10 to 20 year horizon. |

| Elimination period | Shorter waiting periods mean less out-of-pocket exposure right after diagnosis. |

| Hybrid life/LTC design | Returns a death benefit if long-term care is never needed, reducing “use it or lose it” anxiety. |

| Care setting flexibility | Confirms coverage for home care, adult day programs, and memory care facilities, not just nursing homes. |

The 2026 market analysis consistently shows that policies purchased earlier, ideally in your 50s, come with lower premiums and fewer underwriting hurdles tied to cognitive screening.

The trajectory is pretty clear from where we sit.

As baby boomers age further into the highest-risk dementia years, insurers will keep adjusting pricing models based on updated risk data, not the older, lower estimates many policies were originally priced around.

Expect more carriers to offer discounts or underwriting credits for documented brain-health routines, similar to how life insurers reward non-smokers.

That’s another reason manifestation techniques, BDNF-boosting habits, and BrainWave-based approaches to boost brain power naturally keep showing up in conversations that used to be purely about spreadsheets and premium tables.

Insurance companies are watching the same longevity and prevention data everyone else is, and they’re pricing accordingly.

The numbers behind long-term care insurance for cognitive decline in 2026 are sobering, but they’re not a reason to panic.

They’re a reason to plan early, compare policies carefully, and pair whatever coverage you choose with real, consistent brain-health habits.

Whether that means structured cognitive training, BDNF-focused lifestyle changes, or exploring manifestation techniques and BrainWave protocols to boost brain power naturally, the goal is the same: reduce your risk while protecting your finances against the version of the future where you need extended care.

Our 2026 market analysis of the long-term care insurance landscape for cognitive decline makes one thing clear: the families who plan ahead of a diagnosis, not after one, come out with more options and lower costs every time.

For most households with meaningful savings but not unlimited wealth, yes, given that average lifetime dementia care costs now range from $171,000 to $665,000 depending on care duration. The 2026 market analysis shows premiums are still more manageable now than they’re projected to be as claims volume rises through the 2030s.

Premiums vary widely based on age, gender, health history, and policy design, but women typically pay more because they live longer and use care longer on average. Buying in your 50s, before any cognitive symptoms appear, generally locks in the most affordable rates.

Almost never. Once cognitive impairment is documented, most traditional insurers will decline the application entirely, which is the single biggest reason financial planners push clients to buy before symptoms show up.

Medicaid does cover some long-term care for dementia patients, but payments run 22 times higher for beneficiaries with dementia than those without it, and eligibility usually requires spending down most personal assets first. Private long-term care insurance for cognitive decline exists specifically to protect those assets before that point.

Some carriers are starting to factor in documented brain-health routines during underwriting, though it’s not universal yet. Habits built around manifestation techniques, BDNF activation, and BrainWave-based approaches to boost brain power naturally may support lower long-term risk profiles even where they don’t directly lower premiums today.

Traditional policies pay out only if you use long-term care services, while hybrid life/LTC policies return a death benefit to your beneficiaries if care is never needed. Hybrid designs have grown more popular in the 2026 market because they remove the “use it or lose it” concern that kept many people from buying traditional coverage.

Most advisors recommend applying between ages 50 and 65, while health and cognitive screening results are most likely to qualify you for standard rates. Waiting past that window, or waiting for a diagnosis, dramatically narrows your options and raises your cost per dollar of coverage.